by: Mickey Ingles (originally posted on Spin.Ph)

Sports collectibles are having quite a surge recently. Whether it’s sports trading cards or sports nonfungible tokens like NBA Top Shot, the market has been at an upswing.

The collectible industry has been on fire so much that card grader and authenticator Professional Sports Authenticator (PSA) has been forced to suspend most of its operations because of the surge of submissions for grading.

he momentum has even found its way to non-sports collectibles such as graded comics, Pokemon cards, and Marvel trading cards from the ’90s (which is my jam). Critics and skeptics have said that the bubble for collectibles is due to pop soon, but that hasn’t deterred earnest collectors from buying what they can out of sheer nostalgia, investment purposes, or both.

While it’s still uncertain when or if the bubble will pop, one thing is certain though: taxes will have to be paid.

So, how are sports collectibles taxed?

Basic rule: There’s no tax if you don’t sell

The tax hit only happens once the collectible is sold or transferred for consideration. There’s no tax liability for the mere appreciation of value of a collectible, simply because there isn’t any income to begin with.

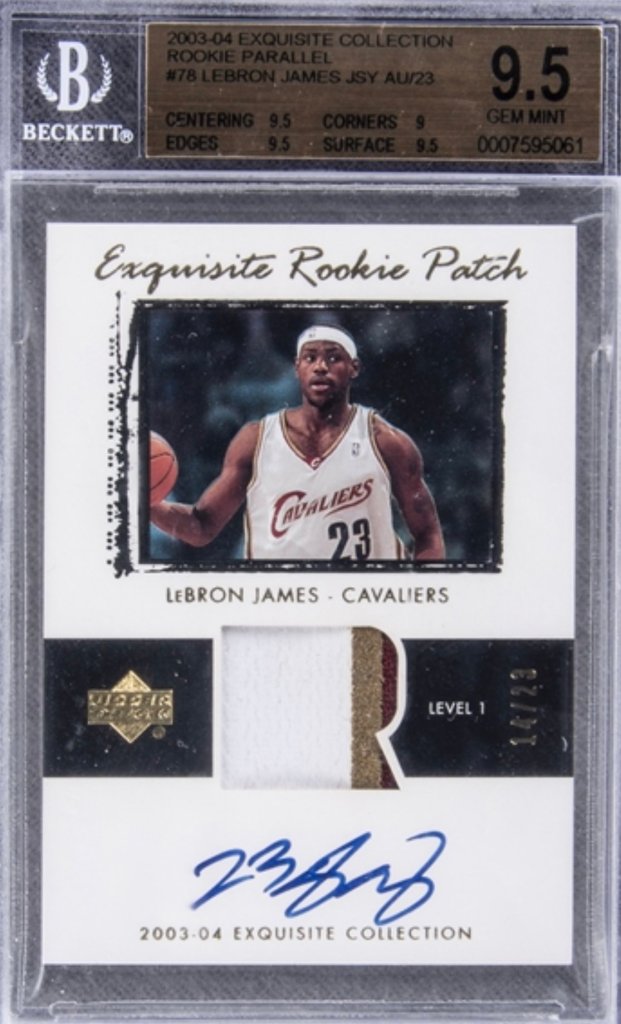

So, if you’ve rummaged through old boxes to find a Trapper Keeper of basketball cards from the ’90s and early ’00s and have the amazing fortune to discover that you owned a Gem Mint 2003-2004 Upper Deck Patch Autograph Parallel Lebron James, don’t worry. You don’t have to pay the taxes on that yet, even if it’s current value once graded is US$1,845,000.

Income tax kicks in once the collectible is sold and there’s a gain on the sale.

So, if you’re not keen on paying income tax, just don’t sell it at all.

Is it an ordinary or a capital asset?

The tax implication of the sale of collectibles will depend primarily on whether the collectible is an ordinary or capital asset.

A collectible is considered an ordinary asset if it’s the kind which would be included in the inventory of a taxpayer at the end of the year, or if it’s property that the taxpayer primarily holds for sale to customers in the ordinary course of business.

In simple terms, if a collectible is sold by someone in the business of selling collectibles, then that’s an ordinary asset.

So, if you’re in the business of buying and selling Top Shot Moments that you were lucky enough to acquire by always getting a good queue number (I’m not jealous, I’m just saying the system is unfair to naturally unlucky people like me, that’s all), those Moments are ordinary assets.

Whatever gain you get from selling a Top Shot Moment will enter your taxable income for the year, which will be subject to the relevant tax rate depending on your tax bracket and/or if you qualify for the 8% gross income tax rate under TRAIN.

As an added bonus, the sale will also be subject to 12% value added tax as it was done in the ordinary course of trade or business, unless your gross annual sales don’t exceed P3,000,000 — which would make you VAT-exempt.

If the collectible is not an ordinary asset, then the law automatically considers it a capital asset.

This is relevant to wily and smart hobbyists who buy collectibles for investment purposes. This is even relevant to clueless collectors who overpaid for Top Shot Moments because they didn’t know any better, didn’t listen to the Bad Shot podcast, got frustrated for missing out on the queue for the nth time, and have the emotional quotient of a hangry snail, a.k.a. me.

Gains from the sale of collectibles classified as capital assets are treated differently from ordinary assets.

First, these aren’t subject to 12% VAT, as these aren’t sold in the ordinary course of trade or business.

Second, the extent of the gain to be computed for income tax purposes will depend on how long the hobbyist has held the collectible. If the collectible has been in the hands of the hobbyist for more than 12 months, then only 50% of the gain will be computed for income tax purposes. If it’s held for less than 12 months, then 100% of the gain will be considered income.

Say, for example, you found a 1986-1987 Fleer Michael Jordan rookie card in your father’s collection a couple of years ago. You had it graded with PSA, and it came back a few months later with that coveted “GEM MT 10” on the label, complete with a chorus of angels singing Hallelujah.

If you sell it for US$150,000, then just 50% or US$75,000 will enter your taxable income because you’ve held it for more than 12 months. If, however, you acquired the MJ rookie card from your pop just a few months back and decide to sell it within the 12-month period, the entire US$150,000.00 will be included in your taxable income.

The lesson for capital assets? Hold it for more than 12 months to take advantage of the 50% incentive.

If you profit from your collectibles, you will be taxed

I know. I know. I may have just ruined the joy of collecting and investing for you by droning on about its tax implications. But be kind. I’m only the messenger in all this.

If you do want to avoid the headaches of dealing with income tax and VAT on your collectibles though, I offer one simple solution: just give me the card, the NFT, the graded comics, the 1990 Impel Marvel Thanos Gem Mint PSA 10. I’m accepting anything to add to my measly collection of ungraded ’90s basketball and Marvel cards, as well as practically worthless Top Shot Moments.

This, of course, is a joke. Giving me collectibles of sizable value will sadly subject you to the payment of donor’s tax.

On that note, happy tax season!

Mickey Ingles is the editor-in-chief of Batas Sportiva. Aside from writing Tax Made Less Taxing, he collects 90s Marvel Trading Cards (and posts them on Instagram) because it brings back awesome memories with his family and is excited to open his first pack of NBA Top Shot moments… although with his luck, he’ll probably just get disappointed again.